Yikes, your clients love everything about the house you showed them except for the dingy tub in the bathroom. Instead of busting their budget by suggesting an expensive new installation, here are some money-saving tips to rescue that tired tub from the scrap heap:

Yikes, your clients love everything about the house you showed them except for the dingy tub in the bathroom. Instead of busting their budget by suggesting an expensive new installation, here are some money-saving tips to rescue that tired tub from the scrap heap:

Quick repairs: If your tub is just discolored or dingy, apply some fiberglass cleaner purchased from your local hardware store to restore its former luster. If the porcelain or fiberglass veneer is chipped, plug the holes with bathtub chip filler — a fiberglass-based compound that comes in matching colors.

Reglazing: This process, costing between $300 and $500, uses high-powered industrial solvents to scour and prepare the tub's surface for a new finish. Most of these finishes are sprayed on and cured chemically with heat lamps. An affordable alternative to replacement, the process lasts up to five years.

Bathtub liner: A method favored by the hotel industry, a bathtub liner can be best compared to crowning a tooth. The existing tub remains in place and is completely covered with a form-fitted acrylic tub liner. Manufacturers, charging between $400 and $600, boast of having molds to fit virtually any tub. Although simple to install, liners slightly reduce tub volume and are less lustrous than porcelain finishes.

Thursday, January 31, 2008

Make Your Tub Sparkle Again!

Wednesday, January 30, 2008

Monday, January 28, 2008

What is going on over there?

"OH ABNER!!!!!"

"OH ABNER!!!!!"

Saturday, January 26, 2008

Tax Deductions for Homeowners

Refinancing points. When you buy a house, you get to deduct points paid to get your mortgage in one fell swoop. When you refinance a mortgage, though, you have to deduct the points over the life of the loan. That means 1/30th a year if it's a 30 year mortgage -- that's $33 a year for each $1,000 of points you paid. Not much, maybe, but don't throw it away. And, in the year you pay off the loan -- because you sell the house or refinance again -- you may get to deduct all as-yet-undeducted points. You do unless you refinance with the same lender. In that case, you add points on the latest deal to the leftovers from the previous refinancing and deduct the expense ratably over the life of the new loan. See more Deductions for Homeowners

Refinancing points. When you buy a house, you get to deduct points paid to get your mortgage in one fell swoop. When you refinance a mortgage, though, you have to deduct the points over the life of the loan. That means 1/30th a year if it's a 30 year mortgage -- that's $33 a year for each $1,000 of points you paid. Not much, maybe, but don't throw it away. And, in the year you pay off the loan -- because you sell the house or refinance again -- you may get to deduct all as-yet-undeducted points. You do unless you refinance with the same lender. In that case, you add points on the latest deal to the leftovers from the previous refinancing and deduct the expense ratably over the life of the new loan. See more Deductions for Homeowners

http://www.mtgfoundation.com/2007/01/mortgage-points-are-often-tax-deductible.html

Open House Sunday

Open House Sunday January 27th 12-130 pm- bring or send your buyers!!

159 Madison 11F $1,147,500 Full listing: http://mail.elliman.com/exchweb/bin/redir.asp?URL=http://www.prudentialelliman.com/877950

Friday, January 25, 2008

When did we start getting the news from a crystal ball?

"I SEE A VERY STRONG...NO WEAK...WELL...YOU BETTER..."

"I SEE A VERY STRONG...NO WEAK...WELL...YOU BETTER..."

OK its time for a rant! I have had just about enough of the "NEWS" lately with the forecasts and the predictions. REPORT SOME FACTS.

Not to disparage our society but we need to get a reality check and stop the madness. We are so misinformed and self serving as a nation. We now think we know a day in advance what the market will do, If Britney will stomp out of court, whether the real estate catastrophe will finally pop, the winner of a caucus and all before we even vote!

Buzz phrases like "the market is going to tank"..."the Mary KATE connection"..."there are thought to be weapons of mass destruction"..."OBAMA WINS!", drive me NUTS.

I was talking to my Mom earlier this week and she referred to a comment that Joy Behar made on THE VIEW. Joy said something to the effect... The trouble with the news is, it isn't news anymore. We used to hear reports of what happened not what was going to happen.

Joy, you have a point! Where is the DATA? When did this transition Happen? WHY IS THIS CALLED NEWS and not The Nightly Predictions with Helen Duncan?

Frankly this is absurd.

People let's get it together, if we all react to these predictions of MADAME WHOSHERNAME... we will be ruled by the suggested, the forced prediction will become reality. Don't Succumb to this... Stand up and make you own moves, Buy- Sell, Invest -Cash In, Vacation-Build a Bomb Cellar, VOTE, PLEASE VOTE...

Do what you want and need not what some "PUNK" Reporter or dilettante on TV tell you to! READ.

Investigate.

Trust Your GUT.

Thursday, January 24, 2008

Wednesday, January 23, 2008

Are bad times, good news?

New Debt City!

How it helped New York boom—and how the bad times now are good news

This article was published in the January 28, 2008, edition of The New York Observer.

Adelaide Polsinelli sells real estate all day for her clients as a top broker at Besen & Associates. She was talking last Thursday about developer and landlord Harry Macklowe’s recent troubles. In February 2007, Mr. Macklowe bought several New York office towers for $7 billion in one of those titanic deals that perfectly reflected this decade’s rowdy, triumphant real estate market.

It was big, first of all: The portfolio included seven prime office towers in Manhattan, North America’s most coveted office market. It had big names: Mr. Macklowe is one of the most well-known landlords in New York, with a portfolio that includes the General Motors Building at 767 Fifth, which he bought in 2003 for $1.4 billion. It involved big amounts: Worldwide Plaza at 825 Eighth Avenue sold for $1.73 billion as part of the deal, the second-biggest building buy in U.S. history.

And, like so much of the recent real estate market, it included a lot of debt.

Mr. Macklowe’s Macklowe Properties put up $50 million for the portfolio; the rest came from lenders. Now, the bills are coming due in early February—one year to the month since the purchase—and “Harry” has put his prized building up for sale: He’s retained ace brokerage CB Richard Ellis to market the GM Building, arguably the world’s most valuable.

Mr. Macklowe is perhaps the most extreme example of real estate debt as the animating factor of the New York City economy right now. Without debt, the city would go broke.

Not exactly, perhaps, but it would be a very different place. It would not be as shiny or as profitable for investment, nor as largely buffeted as it is now from the housing market woes afflicting most of the United States. It would be New York, but it would not be the record New York of the past several years.

Tuesday, January 22, 2008

Federal Reserve makes biggest cut in nearly 24 years...

More information on todays cut:

Fed slashes key rate to 3.5%

Citing weakening economic outlook, Federal Reserve makes biggest cut in nearly 24 years - three quarters of a point.

By Paul R. La Monica, CNNMoney.com editor at large

January 22 2008: 12:02 PM EST

Fed's Emergency Action

Key rates cut 75 basis points

Biggest cuts since Oct. 1984

More cuts expected Jan. 30

NEW YORK (CNNMoney.com) -- The Federal Reserve slashed two key interest rates by three-quarters of a percentage point Tuesday following an unscheduled meeting, citing continued concerns about a weakening economy and turmoil in the financial markets.

The Fed lowered its federal funds rate, which impacts how much consumers pay on credit card debt, home equity lines of credit and auto loans, to 3.5 percent from 4.25 percent.

FULL ARTICLE

http://money.cnn.com/2008/01/22/news/economy/fed_rates/index.htm?eref=rss_topstories

Emergency Rate Cut of .750% to Fed Funds Rate

Open House Finder, The winners are...

After receiving your emails and input at my open houses the winners were a tie! One being the standard NY TIMES online, some still use the paper but the surprise was a site I have had on my blog. It is NATEFIND.

http://www.natefind.com/![]()

I was turned onto this site a few months back by a neighbor. She likes the ease and simple guidance of the site.

Check it out!!

Monday, January 21, 2008

Martin Luther King, Jr.: I Have a Dream

Take a moment and watch this historical speech that was delivered 28 August 1963, at the Lincoln Memorial, Washington D.C.

Sunday, January 20, 2008

Open Houses Manhattan

How do you find open houses?

How do you find open houses?

Do you visit the New York Times?

Individual Company Sites?

Word of mouth?

Inquiring minds want to know!

http://elliman.com/

http://realestate.nytimes.com/sales/NY/Manhattan_County/MANHATTAN_County

http://nymag.com/realestate/sales_oh.htm

http://openhouseny.tv/

Saturday, January 19, 2008

The 80-20 Rule...Changes for The Co-op!

Co-ops Reap Unexpected Bonanza

By VIVIAN S. TOY

Published: January 20, 2008

FOR years, some New York City co-ops that have retail space in their buildings have been doing the unfathomable. They have rented out their commercial space at bargain rents, and to make sure they weren’t making too much money on the spaces, they have even occasionally given back thousands of dollars to tenants at the end of the year.

They have done so because of the 80-20 rule, a federal tax regulation that requires residential co-ops to get at least 80 percent of their gross income from tenant-shareholders and no more than 20 percent from other sources like commercial tenants.

But a change in the law modified those rules late last year, and co-op boards are now busy making sure they are getting every penny possible from their commercial space.

“This change will be a bonanza for co-ops with retail space,” said Richard Siegler, a Manhattan co-op and condominium lawyer. “Co-ops will be able to take in additional income, but the real beneficiaries will be shareholders, because now that buildings can pay expenses with rental income from commercial spaces, shareholders will get lower maintenance charges.”

Friday, January 18, 2008

TOLD YA!!! The next place to buy

After living in this neighborhood for over 10 years, I have sold many apartments in this hood. Always seeing the potential and final frontier for development, the pending HOT NEIGHBORHOOD! Now with every sale I mention all the developments in the neighborhood and what this means for the older condos or coops in this strip. It means return on investment and opportunity!!!From 34th-23rd Street and 5th ave to Park, this is it!

Still undervalued, buy now and in a few years you may actually make more money that you anticipate because of all the anticipated growth in the next few years! Take a look at just a few of the developments in this formerly unknown area. This wont be a gray spot on the map for long, Unless gray is the new black! :)

Take a look at just a few of the developments in this formerly unknown area. This wont be a gray spot on the map for long, Unless gray is the new black! :)

Twenty9th Park Madison - 39 East 29th Street

Urban planners might want to make a case study out of the area just north of Madison Square Park in Manhattan. There's been a persistent stream of development activity in this part of town, and the latest entrant is a rather unremarkable 142 apartment 34-story condo tower rising fast at 32 East 29th Street. Called Twenty9th Park Madison (don't ask) this H. Thomas O'Hara designed condo topped-out in what seemed like record time. It is a plain straight forward design, with a mostly windowed curtain wall, and masonry accents at the base and corners. What interested us more than the building itself (roof deck at right) is whether or not this location will come together as a residential neighborhood. After the jump we consider the area and the neighbors.

The Real Deal reported that Twenty9th Park Madison will have studios through convertible three-bedroom apartments ranging from 536 to 1,309 square feet, with prices starting at $625,000. There will be a lobby espresso bar and cold storage for Fresh Direct delivery.

This lower part of Madison Avenue is very much a neighborhood in transition. During weekdays class-B office space fills the area with workers. At night it tends to empty-out, although that is changing because of all the weak-dollar tourists. Ethnic-day parades take place here on weekends all summer long, many of which were shunted here over the years by city officials precisely because few people lived in the area. But that is changing fast.

To us this still seems way preferable a location to West 42nd Street, where the Orion and the Atelier are located. Those two condo developments got a lot of attention and (apparently) buyers even though they are farther off the beaten path. And we would point out this is much more central than living way down in the financial district. It seems like people are starting to figure it out. Some of the planned or recently completed projects are listed below:

The 200-room Gansevoort Park going up at the corner of 29th Street and Park Avenue South should bring more foot traffic and nightlife.

Jasper - 114 East 32nd Street

Sky House condo

This slim 55 story condo tower has 135 apartments. You can read about it here.

The Parkwood

This is a conversion of a commercial building to full floor condos located at 31 East 28th Street.

Park South Lofts

Another conversion of a mid-block loft building. Located at 45 East 30th Street, the details and setbacks were nicely preserved here. 40 apartments were created here, including a prominent penthouse addition.

M127 by SHoP Architects

Located at 127 Madison Avenue, SHoP Architects radically altered this small commercial building, adding a number of floors and replacing the facade with angled window units that look up the avenue. Loft units are full-floor condos.

176 Madison Avenue

This planned project at 33rd Street will have 69 condo apartments above a mixed use glass and steel tower.

76 Madison is another conversion, this one with an all-glass penthouse added to the top.

http://www.triplemint.com/triplemint/2007/10/twenty9th-park-.html

Thursday, January 17, 2008

HEY HEY HEY! What's happening now!!

Average Sales price decreased to $1.6M from $2.3M

Average Sales price decreased to $1.6M from $2.3M

Sales below $1,000,000 increased to 56% from 43%

Discount from last asking price increased to 2.7% from 2.0%

Discount from original asking price increased to 3.5% from 2.4%

Transactions sold at ask or above increased to 47% from 40%

Median number of days on market from last ask price remains steady at 55 days

Active listings on market have decreased to 8,212 from 8,282

Wednesday, January 16, 2008

Notable Neighborhood!

It's Koreatown! Immigrants Keep It Real, But for How Long? by Lysandra Ohrstrom January 11, 2008

by Lysandra Ohrstrom January 11, 2008

Koreatown’s answer to Bungalow 8 is hidden on the third floor of a shabby commercial building amid the BBQ and karaoke joints lining 32nd Street between Fifth and Sixth avenues.

On a recent Saturday night (verging on Sunday morning), I passed through two layers of doormen and rode a rickety freight elevator up to a futuristic, bi-level, all-white lounge, with translucent glass floors, a two-story waterfall, and thumping techno.

The scene was straight out of a Brett Easton Ellis book by way of Seoul. Twenty-something Korean hipsters sipped martinis from white-leather banquettes in the tunnel-shaped bar, while people sang karaoke from private, plasma-TV equipped rooms upstairs.

Maru opened in 2005 to cater to the younger generation of Korean students and professionals living in condos around Herald Square and embodies the changing dynamics of the neighborhood.

“It was a small town 15 years ago and then, all of the sudden, Koreans started coming to New York,” Maru’s manager, Sonny Lee, explained below the purple and black flashing lights in one of Maru’s karaoke rooms.

“A lot of rich people from Korea send their kids to New York and L.A. to learn English or go to school now, and they spend a lot of money here,” he said.

Sylvia Lee, a broker at CiCi Realty, on Koreatown’s main strip, said young Korean students “love to live in midtown."

“Manhattan for Koreans is what Hong Kong used to be, not British or Chinese, but independent,” explained Ms. Lee. “More money is coming from Korea now and parents are sending their kids to college here, plus Korean currency is doing really well, so there is a higher standard in the neighborhood."

JEMB Properties led the residential transformation of Herald Square when it opened Herald Towers, a 700-unit rental building, in 2000. The Gotham Group followed with the 48-story Atlas rental building on 38th Street in 2002. Pennsylvania-based developer Pitcairn Properties opened the 34-story Magellan in 2003, and the 41-story Tower 31 opened in 2006 on West 31st.

“Since we bought property the whole strip between 23rd Street and 34th Street on Sixth Avenue has turned into a rental residential market,” said Mr. Jerome. “The complexion of the neighborhood changed into a place that is acceptable to live, so rents have ticked up.”

In 2000, rents in Herald Towers were averaging the mid-$30’s a square foot, Mr. Jerome said, and now they are averaging the mid-$50’s.

The Atlas has also seen rents increase from an average of $50 per square foot in 2002 to about $65 a foot now, said Katherine Sabroff the vice president of marketing for the Atlas Group.

Absent from the media buzz surrounding Herald Square’s revitalization is the fate of the small businesses in Koreatown.

The Koreatown of today is certainly a far cry from the 32nd Street of 1982, when the first Korean restaurant opened to feed the city's 100,000-person immigrant community. The buildings on 32nd Street are stacked four floors high with hair salons, Korean art galleries, Internet cafes, bookstores, and shops selling all manner of Asian products--from Korean kitsch to books, movies, and CD's. Most seem geared to younger customers.

Restaurants and shops come and go regularly on 32nd Street, claimed long-time Koreatown employees, save for a few mainstays like the AM record and bookstore on the corner of Fifth. But, aside from a new Pinkberry, most are still Korean-run.

This could change soon, said Mr. Jerome, when long-term leases on 32nd Street expire. He would would not disclose retail rents in JEMB's Herald Center, but said 34th Street has seen a 30 to 40 percent increase since last year.

“Post 9/11 was a different market and if they took them 10 years ago, retail wasn’t that strong then,” he said. “I would think it’s going to be hard for them once leases expire because there’s just so much going on in that neighborhood.”

Tuesday, January 15, 2008

Are you making these Credit Mistakes?

All it takes is one little drop in your credit rating to spark a surge of lender notifications about higher interest rates, lower credit limits and denied applications. Fair Isaac's FICO score, which most lenders use, rates consumers' creditworthiness on a scale of 300 to 850 — 850 being a perfect score. On a $300,000, 30-year fixed-rate mortgage, someone with a solid score of 700 could snag an interest rate of 5.99%, translating to a monthly payment of $1,797. Lose just one point, and you'd get a less favorable rate of 6.27% and pay $19,800 more in interest over the life of the loan.

Ironically, consumers with good credit have more to fear than those who already have a blemish or two on their record. "The higher your score, the farther it can fall," says Craig Watts, a spokesman for Fair Isaac. "[One mistake] suddenly puts you in a very different category of consumer."

To avoid falling from grace, make sure not to make any one of these five mistakes.

Monday, January 14, 2008

What’s Next for New York City Real Estate?

By CHRISTINE HAUGHNEY

By CHRISTINE HAUGHNEY

Published: January 13, 2008

LOOKING back, 2007 was supposed to be the year that the Manhattan residential real estate market slowed down and began to look a bit more like the slumping national market.

Michael Falco for The New York Times

But that didn’t happen. While there were periods when condominiums and co-ops sat unsold because buyers and sellers couldn’t agree on prices, the year ended with the average price of a Manhattan apartment rising to a record $1.4 million, though the number ballooned in part because so many wealthy buyers purchased extraordinarily expensive condos.

No one is predicting that 2008 will be a repeat of 2007. The sprawling pieds-à-terre may still sell for millions at the Plaza and 15 Central Park West, but in general, economists are predicting that prices will drop in some segments of the market and in some neighborhoods around the city.

“New York has had a very good run, and there are still a lot of people sitting around with cash,” said Christopher Mayer, the Paul Milstein professor of real estate at Columbia Business School. “But that doesn’t last forever.”

For full article: http://www.nytimes.com/2008/01/13/realestate/13cov.html?_r=1&ref=realestate&oref=slogin

Sunday, January 13, 2008

RECORD BREAKING TURNOUTS!!!

With all this talk of recession and down sales last week, I am happy to report that the Open Houses I held today had breaking numbers in attendance. I not only ran out of show sheets, but there were and are serious buyers hitting the pavement with or without brokers.

With all this talk of recession and down sales last week, I am happy to report that the Open Houses I held today had breaking numbers in attendance. I not only ran out of show sheets, but there were and are serious buyers hitting the pavement with or without brokers.

As for buyers, a client of mine just secured a rate 0f 5.8% with a 7 year arm!

Saturday, January 12, 2008

OPEN HOUSES 1-13-08

OPEN HOUSE

159 Madison Avenue

159 Madison Avenue 159 Madison Avenue

159 Madison AvenueThe CREDIT CRUNCH

Posted by Noah Rosenblatt on January 11, 2008 at 11.44 AM-

http://www.urbandigs.com/

A: Like I said numerous times, this is NOT A SUBPRIME PROBLEM. This is an overall mortgage + debt problem that extends to alt-a, prime, heloc's, option arm's, cosi/cofi loans, negative amortizing loans, credit cards, auto loans, etc.. Whether you like it or not is an entirely different story. This cycle must play out and that means more pain before we get better. Think of it as a very sick patient that must go through numerous surgeries and rehab before they can get back to normal. Well, we are about to get our 3rd of X number of surgeries and we haven't started rehab yet! When I wrote the Reset Storm post, I tried to explain that we are about enter a painful period where affordability becomes more of a problem as mortgages reset higher, which will further pressure housing, which in turn will further pressure wall street and the securitization of all types of debts: While most are aware of the coming adjustable rate mortgage resets in 2008, I feel like the anticipated severity of the problem is being under-estimated. At a time when new home sales are at a 12 year low, inventories and months supply at highs, we are about to enter a period of time when many struggling homeowners will be hit with payment shock. This is an outright affordability problem both for homeowners & prospective buyers alike; a rare combination. While the second half of 2007 saw many banks/brokerages/lenders/insurers visit the confessional and announce write-downs, 2008 will most likely see the consumers visiting the confessional as they no longer can meet their debt obligations and become delinquent.So far, we only saw the credit crunch sparked by subprime. Now we are starting to hear from credit card companies. As for the Countrywide buyout, I think Hank Greenberg is dead on by stating the fed was behind the deal. If Countrywide had to declare banktrupcy, which they most likely would have been forced to do, it would have been a huge shock to both the tradable markets and consumer confidence. The fed knows this and to think of this deal happening a few years ago, brings regulatory anti-trust questions that likely would have blocked the deal. Not so in today's environment. Lets get to the headlines. AMEX + CAPITAL ONE TO MISS EARNINGS ON CARD LOSSES American Express Co (NYSE:AXP) and Capital One Financial Corp (NYSE:COF), the largest independent U.S. credit card companies, projected profits below analyst forecasts on Thursday, citing mounting consumer loan losses as the U.S. economy slows. The forecasts show how the housing slump, tighter credit, high oil prices and rising unemployment have made it harder for many consumers to pay their bills. This has caused credit problems to widen beyond mortgages and affect other forms of debt, including credit cards and auto loans.MERRILL LYNCH REPORTEDLY FACING MASSIVE WRITE-DOWN The nation's largest brokerage firm, Merrill Lynch & Co., is expected to report losses of $15 billion stemming from soured mortgage investments, according to a published report Friday. The New York Times, citing people who have been briefed on the broker's plans, said the losses would come in nearly double its original estimate, prompting the firm to raise additional capital from outside investors. The losses are expected to be disclosed when the brokerage reports earnings next week, those people said. Merrill is likely to write down the value of its CDO and subprime mortgage-backed security exposures by $10 billion next week, Bernstein Research estimated. Such hits have increased concern that banks and brokerage firms may not be capitalized well enough and sent many companies in search of fresh cash.BANK OF AMERICA TO BUY COUNTRYWIDE FINANCIAL FOR $4 BILLION Bank of America Corp. said Friday it's purchasing Countrywide Financial Corp. for $4 billion, effectively doubling down on a previous investment in the troubled firm and catapulting the buyer into the top spot among mortgage lenders and loan servicers in the U.S. The stock-swap deal will put an end to the independence of the troubled California lender headed by Angelo Mozilo, and represents an increase from the Charlotte, N.C., bank's August investment of about $2 billion.The fact that Countrywide is selling out at these levels indicates serious distress; and BAC already has a vested interest of $2B at $18/share! Hank Greenberg reported yesterday that the Fed was behind the Bank of America / Countrywide deal as bankruptcy rumors started swirling for the troubled lender. Could you imagine the shock to the tradable markets and to consumer confidence that would have occurred if Countrywide declared bankruptcy? They are the nations largest retail lender! According to Greenberg's Marketblog: We’ll know it soon enough, but with the leak that Bank of America is near acquiring Countrywide, several things would appear apparent (at least while we’re playing the guessing game): 1. The Fed is behind the deal.2. The Fed is behind the deal because the rumors yesterday of a near bankruptcy were probably true.3. As part of the deal, the government likely agrees to guarantee BofA against Countrywide-related losses.4. Lost in the in the noise yesterday was that Moody’s downgraded the ratings on 30 (count ‘em — THIRTY!) tranches of Countrywide’s mortgage debt by more than a few notches. They did something similar before American Home Mortgage filed for bankruptcy.5. Investors bid the stock higher assuming a premium when it’s likely that BofA still needs to fully assess the value of the assets before the deal’s full value will be known.6. Big question, of course, is what Countrywide investors will get.7. Rule of thumb with bankruptcies: Stocks often double on their way to zero.8. BofA gets a free bank and a put to the government. This writer agrees that the fed may have been behind this as that would have been news that would have rocked the markets; the last thing we need after an 11% correction!

Friday, January 11, 2008

Thursday, January 10, 2008

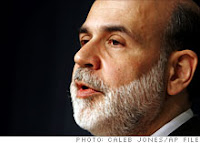

The Fed to the rescue

In a speech Thursday, Federal Reserve chairman Ben Bernanke says central bank ready to cut interest rates again in order to support lagging economy.

NEW YORK (CNNMoney.com) -- Federal Reserve chairman Ben Bernanke said in a speech Thursday that the central bank is prepared to continue lowering interest rates in order to help keep the economy on track.

NEW YORK (CNNMoney.com) -- Federal Reserve chairman Ben Bernanke said in a speech Thursday that the central bank is prepared to continue lowering interest rates in order to help keep the economy on track."We stand ready to take substantive additional action as needed to support growth and to provide adequate insurance against downside risks," Bernanke said in prepared remarks before the Women in Housing and Finance and Exchequer Club in Washington, D.C.

Stocks, which had been trading lower before the speech, rebounded on the news as Wall Street interpreted Bernanke's comments to mean that there is now an increased likelihood the Fed will lower its key federal funds rate by a half of a percentage point, to 3.75 percent, at the conclusion of its two-day meeting on January 30.

To that end, investors are pricing in an 86 percent chance that the Fed will lower rates by a half-point on January 30, according to federal funds futures listed on the Chicago Board of Trade.

Bernanke's speech comes as more and more economists are saying that the economy is either already in a recession or on its way towards entering one. Bernanke stopped short of describing current conditions as a recession in his prepared remarks but he did paint a bleak picture for the economy in 2008.

"Downside risks to growth have become more pronounced. Notably, the demand for housing seems to have weakened further, in part reflecting the ongoing problems in mortgage markets," Bernanke said.

"In addition, a number of factors, including higher oil prices, lower equity prices, and softening home values, seem likely to weigh on consumer spending as we move into 2008," he added.

Bernanke also said that the central bank's new auction program, which it announced in December as a way to loan money to banks in need of cash at a rate below the Fed's discount rate, appears to be a success and could "become a useful permanent addition to the Fed's toolbox."

The Fed has already conducted two auctions for a combined $40 billion and will be loaning $60 billion more later this month through two additional auctions.

THE R WORD

Are we headed into a recession?

Are we headed into a recession?

The central bank chief is due to speak about the housing market later in the day and his comments will be scrutinized for the Fed's latest view on the economy and interest rates. Also on the economic calendar are December same-store sales reports from retailers and a report on wholesale inventories." CNN MONEY

Wednesday, January 9, 2008

Up? Down? Side to Side? Current Market Review

- Overall prices are rising at a very modest pace. The overall median sales price was up 6.4% over the same period last year.

- The luxury market price indicators were up sharply and luxury inventory was down significantly.

- Overall Inventory is down 13.5, but only in co-ops (co-ops down 26.2%, condos 0%)

- Number of sales up 3.2%, a modest increase

- Overall days on market down 12.4% to 131 days

- Listing discount essentially unchanged at 2.7%

Tuesday, January 8, 2008

"CHANGE" of Topic...

The state of the things today is not just focused on any one topic in the media; from Britney and sis to Obama and friends, The"Sub prime Slime"effects and the Starbucks CEO stepping down to let the founder take over once again are all hot topics regarding transformations.

The state of the things today is not just focused on any one topic in the media; from Britney and sis to Obama and friends, The"Sub prime Slime"effects and the Starbucks CEO stepping down to let the founder take over once again are all hot topics regarding transformations.

Friday, January 4, 2008

Maintenance Increases For 2008

The gifts have been exchanged, the ball has dropped, the Christmas trees are on the curb, and the dreaded phrase “maintenance increase” comes knocking on your door. Happy 2008 Co-op Owners!

The gifts have been exchanged, the ball has dropped, the Christmas trees are on the curb, and the dreaded phrase “maintenance increase” comes knocking on your door. Happy 2008 Co-op Owners!

“Maintenance increase” are two words that most co-op owners may not want to hear, but sometimes it is necessary for a building’s board to make the unpopular decision of raising fees. Oil is over 100 bucks a barrel, so fuel is UP UP UP, high operating costs, and insurance rates climbing, plus emergency repairs, they are left with no choice. Although I gulp as I write this, raising maintenance fees often is not only a necessity but advisable.

“It’s totally dependent on economic consistency,” says Jeff Heidings of Siren Management Corp. in Manhattan. “Sometimes it needs to be done, or else there can be serious problems within the building.”

“Having low maintenance fees can be an attractive selling point. Some buildings in Manhattan may pride themselves on not having increased maintenance for decades, but maintenance that’s too low can cause a host of problems on its own—from issues with the 80/20 rule to coming up short in cases of emergency. “

Yesterday, I too received a memo in the mail stating we will be having a 7.5% increase as well as keeping an assessment.

When should you expect an increase?

When there are insufficient funds available to pay the normal operating expenses.

The increase is based on the estimated budget for the upcoming year. The increase is divided by the proportionate shares that each shareholder has.

Higher maintenance costs are not welcomed by the shareholders or the board. The higher costs are something that everyone should accept and understand it is a necessity in the majority of co-ops in Manhattan.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}